Financial Distress and Loss-Making Carriers

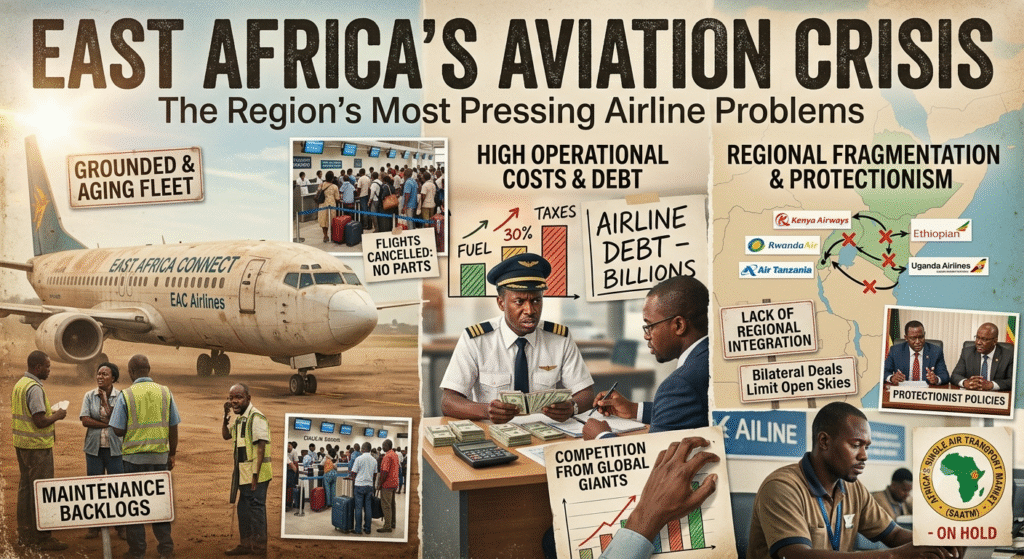

The most fundamental problem facing East African aviation is the precarious financial state of its flag carriers. Kenya Airways, the region’s most prominent airline, returned to losses in 2025 after a brief profit rebound in 2024, driven by prolonged fleet groundings that cut capacity by 20 percent . The airline is heavily indebted and struggling to attract a strategic investor to inject capital needed to stabilise and expand operations .

The situation is mirrored across the region. Uganda Airlines has accumulated approximately $300 million in losses, with grounded aircraft straining operations despite government support . Air Tanzania’s losses rose 64 percent to $34 million in the year ending June 2024, while RwandAir is also struggling with capacity constraints, with four of its 14 aircraft currently grounded .

Aviation expert Dick Omondi, former head of marketing at Kenya Airways, warns of the fundamental flaw in the region’s approach: “Building a hub airport while the anchor airline is loss-making and strategically unsettled would invert cause and effect, and risk creating an expensive underutilised national asset” .

Grounded Fleets and Global Parts Shortage

The shortage of aircraft and spare parts has emerged as a critical constraint, delaying the return of grounded planes across East Africa. Three of the four flag carriers in the region have at least one major aircraft grounded due to engine overhauls or repairs, with a growing backlog at maintenance providers and a scarcity of parts extending downtimes .

The shortage has been driven by a lack of skilled labour and raw materials amid a steep rise in air travel demand following the post-pandemic recovery . Additionally, turbulence in supply chains caused by conflicts in Eastern Europe and the Middle East has further strained delivery of parts. Equipment makers report difficulties accessing key components such as semiconductors, finished castings, and forgings .

African airlines say they are often outbid by richer carriers in developed countries for new aircraft and parts, forcing them to endure longer wait periods. The International Air Transport Association (IATA) warns that more than 1,100 aircraft under 10 years old—3.8 percent of the global fleet—are grounded, compared to just 1.3 percent between 2015 and 2018 .

Soaring Fuel Costs

The war in the Middle East has sent jet fuel prices skyrocketing, hitting East African airlines hard. Ethiopian Airlines CEO Mesfin Tasew said fuel now accounts for more than half of the airline’s operating expenses, up from about 40 percent previously . Jet fuel prices in Addis Ababa have nearly doubled since the escalation of tensions, while average fuel costs across Ethiopian Airlines’ global network have increased by roughly 60 percent .

IATA Director-General Willie Walsh warned that African carriers face a particularly severe burden: “In many African markets, airlines face higher fuel costs, higher airport charges and higher operating costs than carriers in most other regions” . African airlines pay approximately 20 percent more for jet fuel than the global average because of fragmented distribution systems and inefficiencies within the supply chain .

The impact on profitability is severe. According to IATA estimates, African carriers are expected to earn an average profit of about one US dollar per passenger this year despite traffic growth .

Geopolitical Disruptions

Regional conflicts are creating operational nightmares for airlines. The civil war in Sudan resulted in airspace closures that forced carriers to take long, fuel-guzzling detours over Uganda, DRC, Central African Republic, Chad, Niger, Algeria, and then onto Europe—bleeding millions from airline bottom lines .

For Kenya Airways, the situation is compounded by diplomatic tensions. President William Ruto’s embrace of Sudan’s Rapid Support Forces has provoked Khartoum’s fury and alienated powerful states like Saudi Arabia. Sudan banned all Kenyan imports after Ruto’s recognition of the RSF, raising fears that Khartoum could retaliate with flight bans or bureaucratic slow-walking of overflight permissions .

RwandAir was banned from DR Congo airspace over the conflict in eastern DRC, forcing the airline to suspend flights to Abuja, Brazzaville, Cotonou, and Benin . The geopolitical disputes between Kenya and Tanzania have also disrupted aviation, with Tanzania temporarily suspending KQ flights to Dar es Salaam in early 2024 .

Passenger Service Failures

Frequent flight disruptions have become a major source of passenger frustration. A study by the COMESA Competition Commission found that among consumer complaints in the region, delayed flights accounted for 31.71 percent, followed by rescheduled flights (15.43 percent), damaged baggage (11.71 percent), and delayed baggage (10.57 percent) .

Cancelled flights accounted for 9.43 percent, lost luggage and unfair booking conditions at 8 percent, and overbooked flights at 5.14 percent . The study revealed that 71.63 percent of consumers who experienced a cancelled or delayed flight did not receive redress from the airlines .

In response, COMESA has issued comprehensive guidelines requiring airlines to provide refreshments, meals, hotel accommodation, compensation, and re-routing options for affected passengers, with specific provisions for delays of varying durations .

Infrastructure Constraints

Jomo Kenyatta International Airport (JKIA) was designed to handle 7.5 million passengers annually but now processes over 8 million, operating well above capacity . The congestion has been worsened by delays in expansion projects due to lack of funding.

Wilson Airport, East Africa’s busiest general aviation hub, faces its own crisis. The Kenya Civil Aviation Authority has flagged at least 40 buildings obstructing flight paths, with residential and commercial developments encroaching on critical aviation safety zones . Pilots have been forced to adjust approach and departure techniques due to altered wind patterns and visual obstructions .

Regional Competition and Gulf Carriers

East African airlines face intense competition from Gulf carriers that dominate regional connections . Qatar Airways, Emirates, and Turkish Airlines have established strong footholds in the region, offering extensive global networks and modern fleets that regional carriers struggle to match.

Ethiopian Airlines, which has a fleet of about 170 aircraft serving more than 160 passenger destinations, has maintained dominance over trunk routes, giving it an edge over regional airlines which have less than half its fleet size .

Liberalisation Stalled

The failure to fully implement Open Skies agreements continues to constrain the region’s aviation potential. Many African states have been reluctant to implement the Fifth Freedom of the Air, which allows airlines to pick up passengers travelling between two foreign countries on a single route . Without this, East African carriers cannot offer cost-effective stopovers that would reduce fares and improve connectivity .

The East African Community has drafted regulations to liberalise air transport, but these remain pending adoption . Without implementation, travel costs remain among the world’s highest, and intra-African connectivity remains stunted.

Currency Volatility

Currency volatility adds another layer of financial pressure. As IATA’s Chief Economist noted: “You can have up to 80 percent of your costs denominated in US dollars while most of your revenues are earned in local currencies. When exchange rates move against you, the financial impact can be significant” .

This imbalance is particularly difficult for airlines operating in emerging markets where local currencies can weaken against the dollar, forcing carriers to increase fares, reduce capacity, and even postpone investment .

The Path Forward

Despite these challenges, there are glimmers of hope. Kenya is implementing reforms, modernising airport infrastructure, and strengthening connectivity to restore its position as East Africa’s leading aviation hub . Ethiopia’s Bishoftu Airport project and Ethiopian Airlines’ ambitious expansion demonstrate what is possible with strategic vision and financial discipline .

Industry leaders stress that achieving the region’s aviation potential will require resolving the fundamental imbalance between airport infrastructure and airline viability. As Sean Mendis, former chief operations officer of Africa World Airlines, noted: “The reality is that neither side can build an aviation hub without the cooperation of the other. The airline drives the process while an airport facilitates it” . For East Africa, the path forward requires coordinated action on financing, regulation, infrastructure, and geopolitical stability.