The Turbulent Skies: Africa’s Airlines Struggle Amid Deep Challenges

Africa’s airline industry sits at a crossroads of promise and persistent struggle. While demand for air travel on the continent is growing faster than most regions globally, African airlines continue to operate in one of the most challenging and expensive environments in the world. Airlines face high costs, limited connectivity, financial pressures, aging fleets, and a fragmented market that undermines profitability and sustainable growth. (IATA)

A Sky Full of Hurdles: Structural Problems

1. High Operating Costs

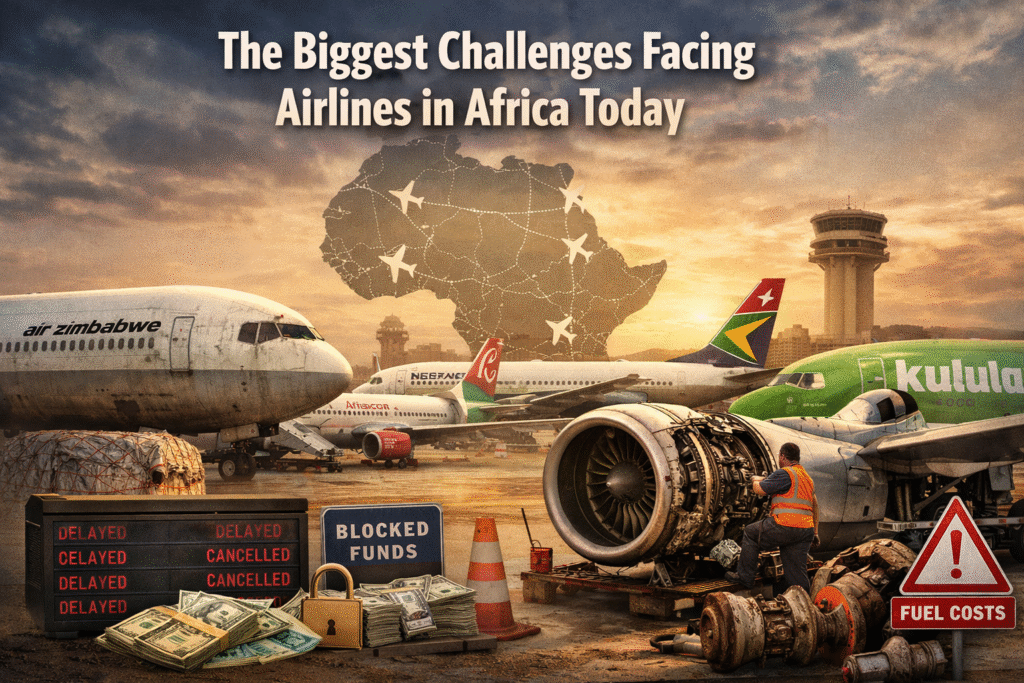

African airlines operate in a costly environment compared with global peers. Jet fuel in the region can cost up to 17% more than the global average, with limited refining capacity forcing many carriers to import expensive fuel. Taxes and aviation charges—including navigation fees and airport tariffs—are often significantly higher than in other regions, eroding margins and inflating ticket prices. (Travel And Tour World)

These elevated costs are compounded by higher maintenance and insurance costs, making it harder for African carriers to reinvest in operations or scale effectively. The result is an expensive cost base that leaves airlines in Africa with the lowest profit margins in the world—just around 1.3% forecast for 2026, compared to an average of nearly 4% globally. (IATA)

2. Blocked Funds and Foreign Exchange Constraints

A particularly acute problem is the issue of blocked funds—revenues that airlines cannot repatriate or convert into hard currency. As of late 2025, Africa accounted for roughly 79% of global blocked airline funds, amounting to nearly $1 billion. Airlines are restricted by governments from converting earnings into dollars or euros, which creates cash-flow bottlenecks and hampers their ability to pay for essential inputs like fuel, aircraft leases, and insurance. (eplaneai)

This foreign exchange stress forces airlines to reduce or suspend services in key markets to preserve scarce hard currency, undermining network reliability and competitive positioning.

3. Fragmented Markets and Limited Connectivity

Intra-African aviation remains deeply fragmented. Only about 19% of routes within Africa are served by direct flights, forcing many travelers to fly through distant hubs in Europe or the Middle East even when traveling between neighboring African cities. Protectionist bilateral agreements and slow implementation of liberalization policies like the Single African Air Transport Market (SAATM) keep market barriers high and competition low. (eplaneai)

Without scale or deep networks, many African airlines struggle to achieve the economies of scale needed to lower unit costs and attract price-sensitive passengers.

Aging Fleets and Supply Chain Woes

Another significant structural hurdle is the age of aircraft operated by many African carriers. On average, African airlines fly older aircraft than global competitors, leading to higher fuel consumption, more frequent maintenance, and expensive downtime. Aging fleets also make airlines less attractive to business travelers and limit long-haul competitiveness. (Travel And Tour World)

Complicating this is a global shortage of aircraft parts. Airlines such as Uganda Airlines, Kenya Airways, Air Senegal, and RwandAir have been forced to ground aircraft due to delays in receiving spare parts, leading to cancellations and reduced schedules. This supply chain crunch is part of a broader, industry-wide bottleneck that is disproportionately felt in Africa. (Africanews)

Individual Airlines Under Pressure

While the industry’s challenges are broad, some carriers exemplify the specific problems facing African aviation today.

South African Airways (SAA)

Once a flagship carrier with global reach, South African Airways has endured years of financial instability. After entering bankruptcy protection in the late 2010s, SAA scaled back its fleet and slashed routes to cut losses. Even today, the airline is rebuilding its operations under government ownership after major restructuring efforts. (Wikipedia)

Air Zimbabwe

Air Zimbabwe typifies decades of financial turmoil. The national carrier was repeatedly suspended due to unpaid debts and foreign exchange shortages, with inflation and currency crises forcing service cancellations and mass layoffs. While the airline has recently sought to rejoin global distribution systems, its ability to sustain regular international service remains fragile. (Wikipedia)

FastJet and Low-Cost Carriers

Low-cost carriers (LCCs) like FastJet face even steeper odds. Their business models depend on efficient operations and rapid growth, but foreign exchange risk, limited domestic demand, and competition from larger carriers hinder expansion. LCCs represent only a small fraction of Africa’s seat capacity—around 5%, compared with 40-45% in Europe and Asia—limiting affordable travel options. (AGN)

Kenya Airways: A Slow Recovery

Kenya Airways has been on a long road to recovery after years of losses and heavy debt. While it reported a profit in 2024 for the first time in over a decade, the airline still relies heavily on government support and needs fleet modernization to sustain growth. (Reuters)

Kulula.com and Historic Failures

Other airlines like Kulula.com and Mango (subsidiaries of South African carriers) have ceased operations entirely due to financial collapse or restructuring. These closures reflect how fragile airline economics can be in an environment where even established carriers struggle to break even. (Wikipedia)

Impact on Passengers and the Broader Economy

The challenges facing African airlines translate directly into higher fares, limited routes, and unreliable service for passengers. Air travel remains disproportionately expensive within Africa, often costing more than equivalent routes in Europe or Asia. As a result, many Africans still travel via hubs like Istanbul, Paris, or Dubai—even for journeys between two African cities. (The Guardian)

For economies dependent on tourism and trade, weak air connectivity constrains growth. Businesses face higher logistics costs, and tourism markets struggle to attract visitors when flights are expensive, infrequent, or non-existent.

Glimmers of Hope and Future Prospects

Despite these challenges, there are signs of resilience. Demand for air travel continues to grow, infrastructure investments are underway in countries like Ethiopia, and some airlines are modernizing their fleets. Implementation of policies like the Single African Air Transport Market could unlock greater competition, lower fares, and more routes if fully realized.

But for African aviation to truly take off, carriers must overcome deep structural hurdles—high costs, regulatory fragmentation, foreign exchange constraints, and supply chain bottlenecks. Strengthening regional cooperation, investing in maintenance and training facilities, and fostering a business environment that supports airline profitability will be essential steps forward.