Nairobi, Kenya — As the sun rises over the skyscrapers of Nairobi’s Upper Hill district on a crisp April morning in 2026, a different kind of dawn is breaking across East Africa. It is not merely the start of another business day; it is the beginning of what many analysts are calling a “decisive decade” for the region’s economy. While much of the developed world grapples with stagnant productivity and geopolitical fragmentation, East Africa is emerging as a surprising bright spot—a land of billion-dollar infrastructure bets, surging private capital, and a youthful workforce ready to leapfrog legacy industries.

Yet, for every CEO shaking hands at a conference in a glass-walled hotel, there is a truck driver stuck at a border post for three days due to an “unpredictable” tax regime. For every financier celebrating a 30% rise in deal volume, there is a manufacturer struggling to find affordable long-term credit. The story of business in East Africa today is a tale of two realities: record-breaking economic potential tangled in the red tape of incomplete regional integration .

The Macroeconomic Boom: Africa’s Growth Engine

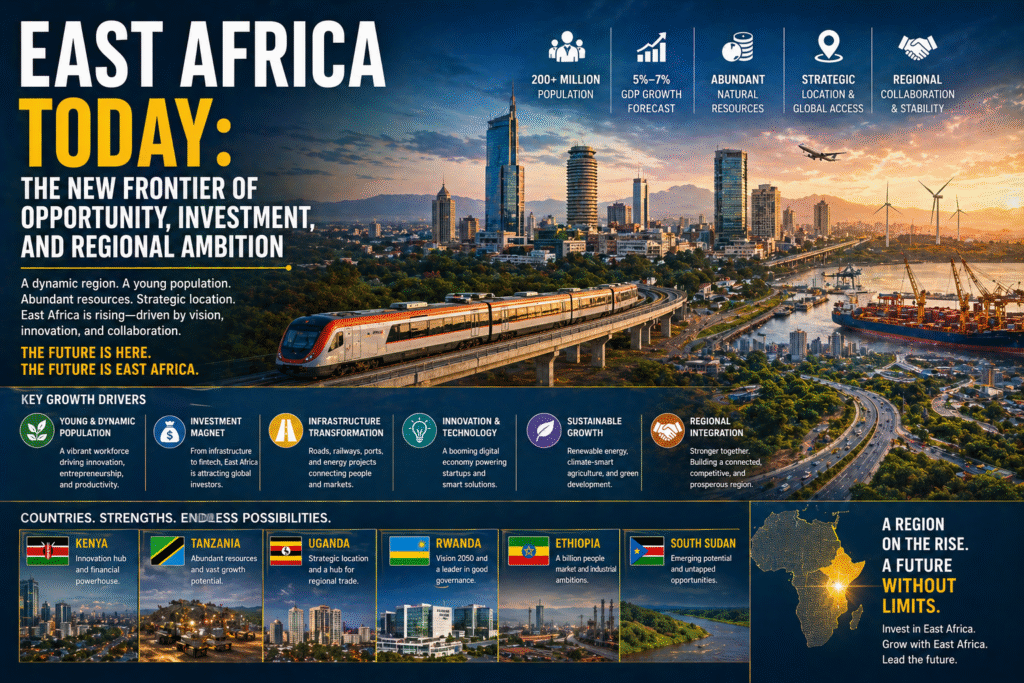

According to the United Nations’ World Economic Situation and Prospects 2026, East Africa is projected to be the continent’s fastest-growing subregion, with GDP expected to expand by 5.8% in 2026 . This growth outpaces the African average of 4.0% and leaves the global north in the dust. The drivers of this acceleration are no longer just about aid dependency or raw commodity extraction; they are structural.

Ethiopia and Kenya are the twin engines. Ethiopia, despite past internal conflicts, is projected to grow at 6.3% this year, fueled by sweeping currency and financial-sector reforms unrolled since 2024 . The International Monetary Fund recently approved a $261 million disbursement for Addis Ababa, praising “better than anticipated macroeconomic outcomes” . Simultaneously, Kenya’s diversified economy—spanning tech, agriculture, and services—is expected to grow at 5.1%, supported by strong foreign reserves and a stabilizing shilling .

But growth figures alone don’t tell the full story. For the first time in a generation, local institutional investors are stepping up to fill the void left by retreating Western donors. As Jane Nzau, a pension administrator at the Central Bank of Kenya, recently put it: “Pension funds in Kenya are ready to invest and provide long-term capital, provided there is structure, proper regulation, and good returns” .

The Capital Surge: $4.1 Billion and the Private Credit Revolution

The numbers emerging from the 22nd Annual AVCA Conference, held in Nairobi at the end of April, are staggering. Between 2021 and 2025, East Africa attracted a cumulative $4.1 billion in investments . This influx is not just coming from the usual suspects—London or New York. It is coming from a sophisticated ecosystem of African finance giants, including the Africa Finance Corporation, British International Investment, and a host of local pension funds looking for yield .

One of the most significant shifts is the explosion of private credit. As banks remain cautious, private debt has become the bridge for growing enterprises. Deal volume in this sector rose 30% year-on-year, with East Africa now accounting for 36% of Africa’s total private debt transactions . This is a maturation of the market; businesses are moving away from informal lending and toward structured, regulated growth capital.

However, the capital is picky. Investors are crowding into frontier markets like Uganda, Tanzania, and Rwanda, but Kenya remains the “core deployment” hub due to its relative stability and liquidity . The signal is clear: East Africa is open for business, but only where governance holds up.

The Regional Puzzle: Integration vs. Protectionism

If there is one word that dominated business leader panels in the first quarter of 2026, it is frustration. Despite the existence of the East African Community (EAC) and decades of rhetoric about a common market, intra-regional trade remains stubbornly low, accounting for less than 15% of total commerce—far below the 40% target set for the end of the decade .

At the East African Business and Investment Summit in Nairobi in February, the private sector delivered a blunt ultimatum to politicians. “Frameworks exist, but implementation gaps persist,” warned John Lual Akol, chairperson of the East African Business Council . He urged governments to move from reform to tangible results.

The barriers are often invisible but deeply expensive. A truck carrying maize from Uganda to South Sudan might face dozens of unofficial checkpoints. A Kenyan tech consultant working in Tanzania might need multiple work permits. These non-tariff barriers, coupled with unpredictable tax regimes, are the silent killers of East African competitiveness .

Yet, there is cautious optimism. Kenya and Tanzania—historically rivals—have reaffirmed a commitment to deepen ties, with trade between them now exceeding $1 billion annually . The two nations are focusing on energy and industrial investment, signaling a move away from zero-sum competition toward synergistic growth.

The Infrastructure Gamble: Mega-Airports and Energy Corridors

East Africa is currently the site of some of the most ambitious infrastructure projects on the planet, signaling a long-term bet on logistics and manufacturing.

In Ethiopia, earthworks are underway for the $12.5 billion Bishoftu International Airport, which Prime Minister Abiy Ahmed has dubbed “the largest aviation infrastructure project in Africa’s history” . The goal is to transform Ethiopia into a global logistics hub, leveraging its geographic position and national airline’s dominance.

Similarly, Kenya is pushing forward with a long-delayed $1.5 billion upgrade of Jomo Kenyatta International Airport (JKIA) in Nairobi, involving partners from Qatar . This is paired with extensions of the Standard Gauge Railway (SGR) and new road networks designed to turn Nairobi into a seamless gateway for imports and exports.

But these shiny projects mask a deeper vulnerability: a lack of affordable long-term finance. The African Development Bank warns that the continent faces a persistent gap in long-dated capital. While Ethiopia’s Public-Private Partnership (PPP) program is advancing solar and housing projects, the biggest bets still rely on sovereign guarantees and concessional loans .

The Risk Landscape: Elections, Debt, and Forex

No review of East African business in 2026 would be complete without acknowledging the shadows. The region is navigating a complex electoral calendar. Kenya is heading into a major election cycle in 2027, and Ethiopia is managing the political fallout of recent peace deals, which creates policy uncertainty for investors .

Furthermore, the era of cheap Western aid is ending. Donor countries are scaling back, leading to financial strain at the EAC headquarters in Arusha, where delayed member contributions have even suspended parliamentary sessions . This is forcing the region to look inward. The EABC has unveiled a roadmap for economic self-reliance, focusing on formalizing informal employment and boosting intra-African trade under the African Continental Free Trade Area (AfCFTA) .

Perhaps the most immediate risk is foreign exchange volatility. While Ethiopia’s reforms have opened up the forex market, a dangerous gap remains between official bank rates and the parallel market, creating uncertainty for importers and banks .

Conclusion: The Momentum is Real, But So Are the Obstacles

Standing at the midpoint of 2026, East Africa is a region of immense contrasts. In the boardrooms of Nairobi and Kigali, the mood is electric; private capital is flowing, GDP is rising, and the infrastructure of the future is breaking ground. Kenyan CEOs are actively planning acquisitions in Tanzania, Uganda, and Rwanda, signaling a belief in a shared destiny .

But on the ground, the reality is messier. The promise of a “Single Customs Territory” remains unfulfilled. The cost of capital is high, and the road to integration is riddled with bureaucratic potholes.

For the business leader, the equation is simple: East Africa offers some of the highest returns on the planet, but those returns require patience, local knowledge, and a tolerance for chaos. As the UN notes, while the growth forecast of 5.8% is impressive, it still falls short of the 6.3% average seen in the decade before the pandemic . The runway is long, but for those willing to navigate the turbulence, the East African sky is the limit.