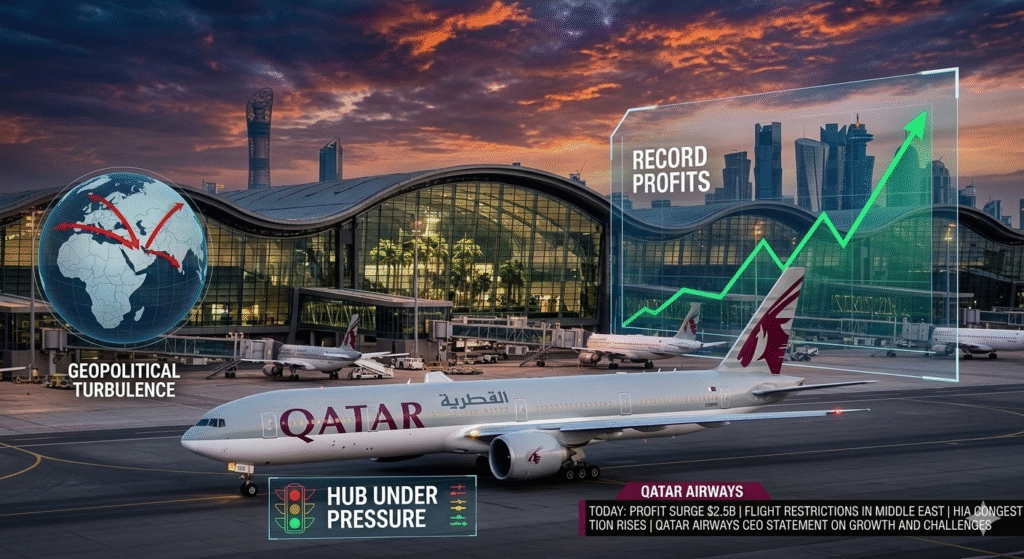

In the space of a single week in March 2026, Qatar Airways has embodied the duality of modern aviation: simultaneously celebrating its most profitable year in history while suspending all flights as regional conflict closes the airspace above its Doha hub. This is the reality for the Gulf’s super-connectors—massive commercial success built on a foundation of geopolitical vulnerability.

The state-owned carrier reported a record $2.15 billion profit for its last fiscal year, carrying 43.1 million passengers on revenues of $23.4 billion . Yet as of March 5, 2026, the airline is operating only limited relief flights for stranded passengers, its core network grounded by the closure of Qatari airspace amid the escalating US-Israel conflict with Iran . This is Qatar Airways today: financially stronger than ever, operationally grounded, and racing to support passengers while awaiting permission to fly again.

Part 1: The Record-Breaking Financial Story

Let us begin with the achievement, because it is substantial. The Qatar Airways Group reported a 28% increase in profit to $2.15 billion for the fiscal year ending March 2025, up from $1.6 billion the previous year . Revenue climbed 17% to $23.4 billion, driven by record passenger numbers and strong cargo performance .

Group CEO Badr Mohammed Al-Meer framed the results as a testament to organizational culture and strategy: “These record-breaking results are a testament to the hard work, skill and dedication of teams across all of Qatar Airways Group. I know that none of the outstanding results we’re announcing today would be possible without our people – more than 55,000 of them across the globe – and it’s our focus on fostering that talent, which has been a core focus of our Qatar Airways 2.0 strategy” .

The financial performance places Qatar Airways among the world’s most profitable airlines. While Dubai-based Emirates reported a staggering $5.2 billion profit , Qatar’s results demonstrate that its hub model—connecting East-West traffic through Doha—remains structurally sound and commercially viable.

The Qatar Airways Group encompasses not only the airline but also its cargo division, the country’s airport operator, and Qatar Duty Free . This integrated structure enables the group to capture value across the aviation ecosystem, from passenger tickets to airport retail to cargo logistics. Cargo revenue alone increased 17% in the 2024-2025 financial year, highlighting the growing importance of yield optimization and commercial strategy over pure tonnage growth .

Part 2: The Fleet and Network Strategy

Qatar Airways currently operates a fleet of over 230 aircraft, a mix of Airbus and Boeing long-haul and medium-range planes . But the fleet is growing. As of March 2025, the airline had 292 aircraft including passenger jets, freighters, and executive jets, with 202 aircraft committed for delivery, including 45 scheduled within one year .

The widebody strategy is central to Qatar’s ambitions. The carrier expanded its Boeing 777X order in 2024 and followed with a major widebody agreement in 2025 covering up to 210 aircraft, primarily Boeing 787s and 777Xs . These orders serve dual purposes: growth and fleet renewal.

However, programme delays introduce uncertainty. Continued slippage in the Boeing 777X timeline means capacity planning must account for potential delivery shifts into 2027 . To maintain regional connectivity and hub feed economics, Qatar Airways plans to introduce high-density A321neo aircraft ahead of full narrowbody deliveries, expected to begin in 2026 .

Network breadth remains a competitive differentiator. The airline serves more than 170 destinations worldwide and continues expanding secondary city connectivity while maintaining high load factors. Membership in the oneworld alliance strengthens market reach, loyalty value, and connectivity beyond the airline’s own network .

Strategic equity partnerships are extending the airline’s reach without replicating short-haul operations. Qatar Airways has acquired stakes in Virgin Australia and Airlink, securing regional feed and connectivity in key markets .

Part 3: The Infrastructure — Hamad International Airport

The airline’s success is inseparable from its home: Hamad International Airport, named the ‘Best Airport in the Middle East’ for 11 consecutive years and ‘World’s Best Airport Shopping’ for the third year running by Skytrax . The airport has previously been named the ‘World’s Best Airport’ in 2021, 2022, and 2024 .

Passenger throughput reached 54.3 million in 2025, a 3% year-on-year increase from 52.7 million in 2024 . This represents a transition from post-pandemic recovery to managed growth, with the airport operating in the mid-80% range of its capacity.

Crucially, traffic composition is shifting. Point-to-point traffic—passengers whose journey begins or ends in Doha, rather than connecting through it—reached 13.5 million passengers in 2025, up from 12 million the previous year . This suggests Doha’s origin and destination base is expanding alongside its traditional transfer flows, adding resilience to the hub model. Local traffic growth may help flatten peak connection waves and improve operational resilience .

Infrastructure constraints are easing structurally. The opening of Concourses D and E in March 2025 increased the airport’s capacity to more than 65 million passengers annually, expanded terminal space to 845,000 square metres, and raised the number of contact gates to 62 . Future constraints are therefore more likely to stem from peak wave scheduling, stand availability, and airspace variability rather than terminal limits .

Cargo performance remains strong. Airport volumes reached 2.6 million tonnes in 2024 before easing slightly to 2.59 million tonnes in 2025 . This marginal decline aligns with global freight trends, but Qatar Airways Cargo’s 17% revenue increase demonstrates the value of yield optimization over pure volume growth .

Part 4: The Grounding — Geopolitical Reality Intervenes

This brings us to March 2026—and the stark reminder that even the most successful airline cannot fly when its airspace is closed.

On February 28, Qatar Airways announced the temporary suspension of all flights due to the closure of Qatari airspace following regional developments . Explosions were reported in Doha amid the escalating US-Israeli attacks on Iran . The carrier has extended the suspension multiple times, with the latest update on March 4 indicating flights remain suspended and a further update will be provided on March 6 .

The airline has been clear about the conditions for resumption: “Qatar Airways will resume operations once the Qatar Civil Aviation Authority announces the safe reopening of Qatari airspace” .

In response, the carrier announced on March 5 that it will operate limited relief flights to support stranded passengers . The planned services include:

- From Muscat to London Heathrow, Berlin, Copenhagen, Madrid, Rome, and Amsterdam

- From Riyadh to Frankfurt

The airline is contacting affected passengers directly with assigned flight details and travel arrangements . It has urged passengers not to proceed to the airport unless they have received official notification, and to update their contact details through the website or mobile app .

This is not Qatar’s first experience with geopolitical disruption. During the 2017-2021 diplomatic rift with Saudi Arabia, the UAE, Egypt, and Bahrain, the airline lost access to 18 Middle East cities and was banned from their airspace, forcing longer routes and higher fuel costs . That experience developed institutional capabilities for managing crisis—capabilities now being tested again.

The grounding highlights what analysts describe as the “highest impact risk” to Qatar’s hub model: geopolitical shocks . As Aviation Business Middle East noted in its February 2026 outlook, “Temporary regional airspace closures in 2025 triggered mass cancellations and stranded passengers, highlighting the vulnerability of global transit networks during acute disruptions” .

Part 5: The Outlook — Resilience Tested

For 2026, the outlook for Qatar Airways is favourable but conditional. Regional fundamentals remain strong, with IATA projecting Middle East carriers to lead global net profit margins . However, Qatar’s highly international hub model remains exposed to geopolitical disruptions and policy shifts in key external markets .

Regulatory risk stems primarily from external market access rather than domestic policy. The EU-Qatar open skies agreement remains politically sensitive, and potential restrictions could affect connectivity into a core long-haul market .

Sustainability initiatives continue to advance but remain limited in scale. Qatar Airways has secured sustainable aviation fuel supplies through targeted agreements and longer-term offtake commitments, aligning with industry net-zero ambitions. However, SAF availability and aircraft delivery delays continue to challenge decarbonisation timelines .

Industrial capability development is emerging as a strategic advantage. Qatar Airways has been selected by Honeywell as an official A350 auxiliary power unit maintenance provider for the Middle East and Africa . Meanwhile, collaboration between Qatar Airways and Qatar Free Zones Authority aims to build an integrated MRO and logistics ecosystem linked directly to Hamad International Airport and Hamad Port. As widebody growth increasingly depends on maintenance capacity and parts availability, these initiatives strengthen operational resilience .

Conclusion: The Paradox of Modern Gulf Aviation

Qatar Airways in March 2026 embodies the paradox at the heart of Gulf aviation. The business model works spectacularly well: a modern hub, a young fleet, a global network, and record profits. The airline has demonstrated that it can navigate diplomatic isolation, pandemic disruption, and intense regional competition.

Yet all of this depends on a single assumption: that airspace remains open. When that assumption fails—as it has in the past week—even the world’s most profitable airline must park its fleet and wait.

The relief flights now operating from Muscat and Riyadh represent a limited but essential response: getting stranded passengers home while the geopolitical situation stabilizes. The airline’s statement that it will “continue to closely monitor the situation and will share further updates as soon as they become available” reflects the only honest answer available when forces beyond commercial control intervene.

When normal operations resume—and they will resume—Qatar Airways will return to its core mission: connecting the world through Doha, carrying millions of passengers, and building on the record profitability it has achieved. But the events of March 2026 serve as a reminder that for airlines based in the Gulf, commercial strategy cannot be separated from geopolitical reality.

The hub model is structurally sound, financially successful, and strategically vital to Qatar’s economic diversification. It is also, and will remain, vulnerable to forces no airline can control. Managing that vulnerability—through fleet flexibility, network diversification, and crisis response capability—is now as central to Qatar Airways’ success as its award-winning service and world-class hub.

For now, passengers wait, the airline communicates updates, and Doha’s airspace remains closed. The record profits will matter again when the flying resumes. Until then, Qatar Airways is focused on what matters most: getting its passengers home safely when the skies finally reopen.